Loading...

Case Study — Fintech / Algorithmic Trading

We Built an Algorithmic Backtesting Engine That Tells the Truth About a Strategy in Seconds

A private trading firm was manually backtesting Smart Money Concepts setups on TradingView — slow, biased, and impossible to scale. We replaced hundreds of hours of manual replay with a custom engine that runs any SMC model across three years of data in seconds and reports its real, unvarnished edge.

The verdict, in full: win rate, net P&L, profit factor, drawdown and streaks computed across 70,135 fifteen-minute bars of XAUUSD.

70,135

Bars Analyzed

45

Trades Simulated

+$3,000

Net P&L

Seconds

Run Time

The Dashboard

A Complete Backtesting Command Center

Traders configure every parameter of their strategy — entry logic, multi-asset selection, kill zones, risk and news filters — then get an instant, data-backed verdict. Here is a full run, end to end.

Tested onXAUUSD·21 Jun 2023 → 10 Jun 2026·70,135 × 15m bars·Model A (ICT Reference), 1:3 R:R

1

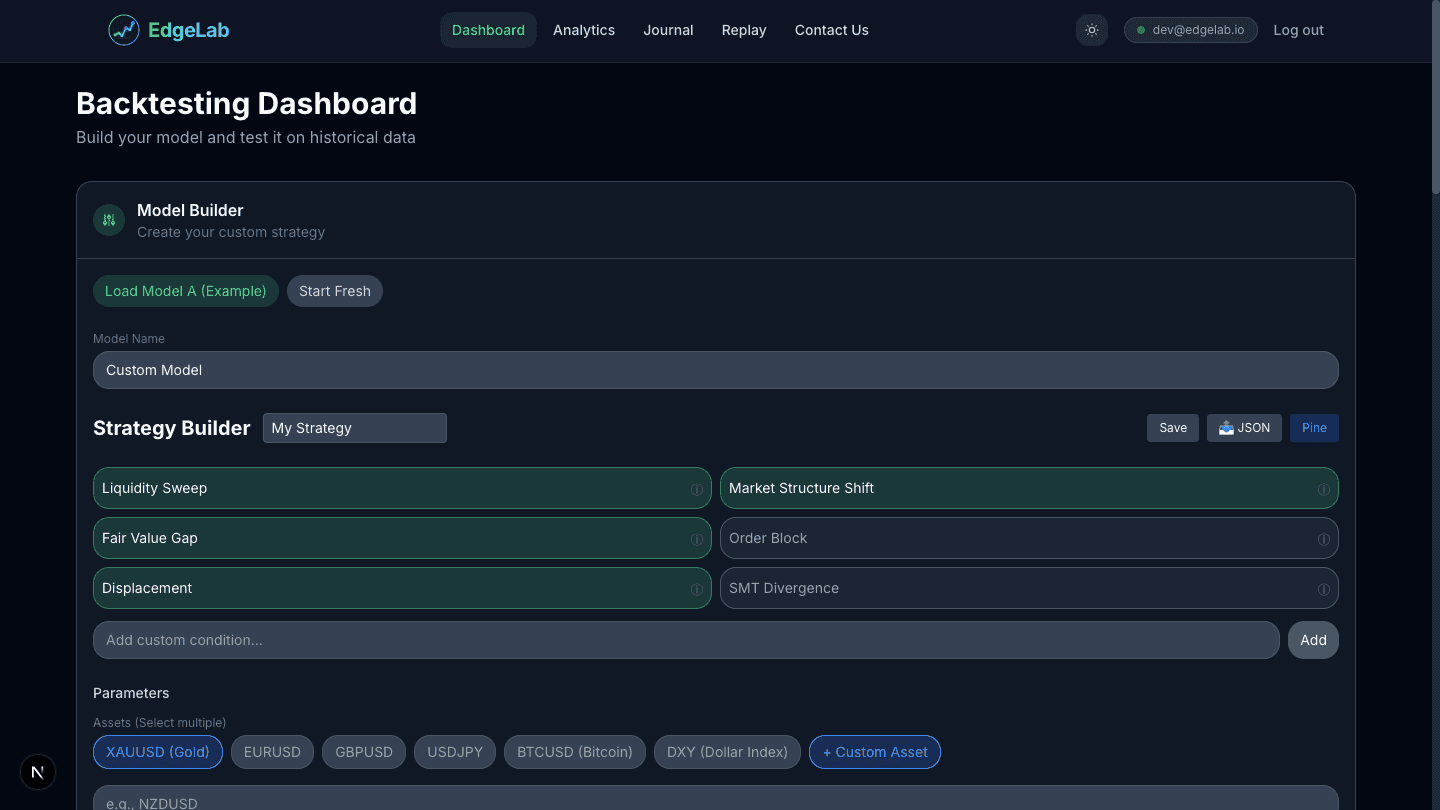

Strategy Builder

Compose the model from SMC primitives — Liquidity Sweep → Market Structure Shift → Fair Value Gap → Order Block → Displacement (2×). Save it, or export to JSON and Pine Script.

2

Multi-Asset Parameters

Pick assets (XAUUSD, EURUSD, GBPUSD, USDJPY, BTCUSD, DXY), execution timeframe, target R:R and data window — up to three years back.

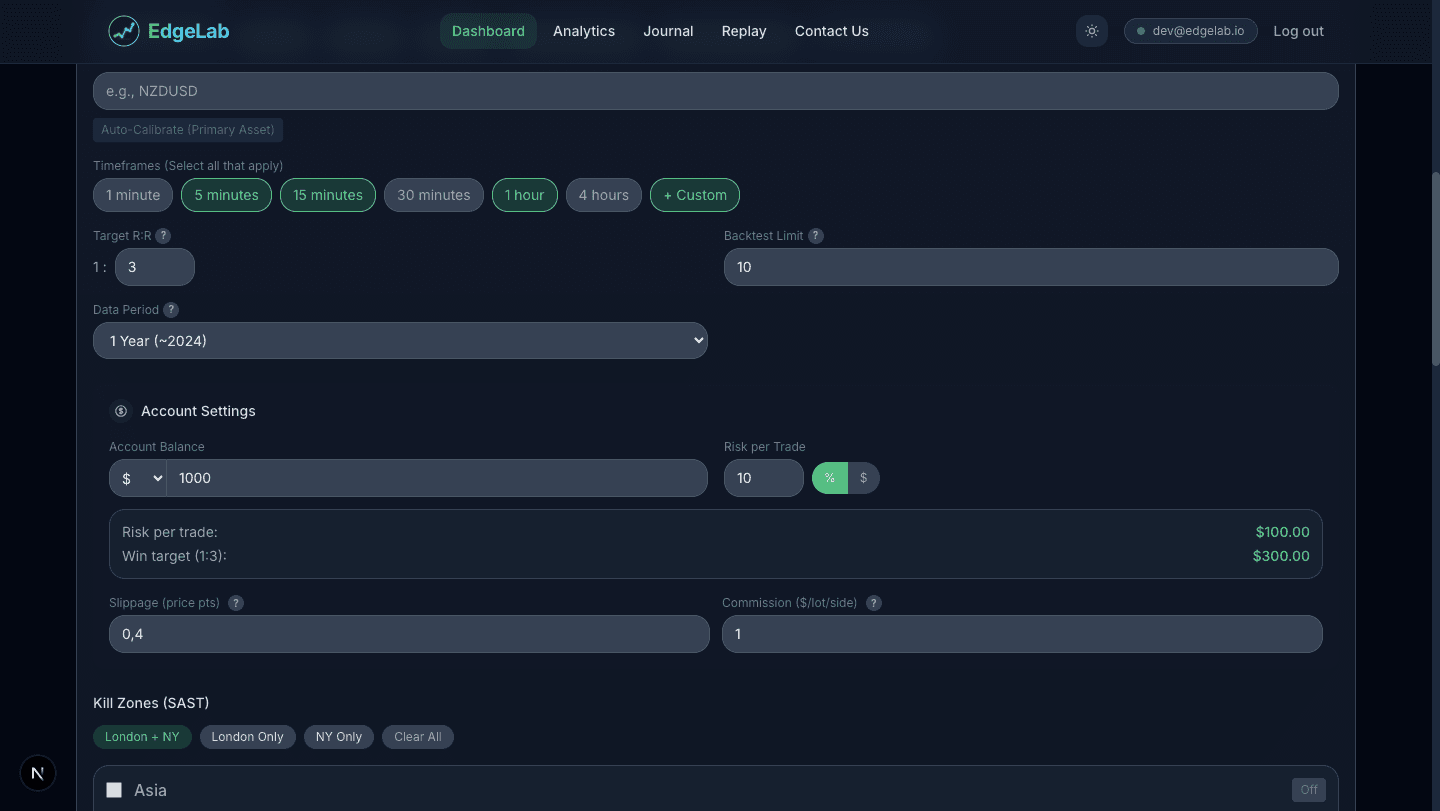

3

Risk, News & Kill Zones

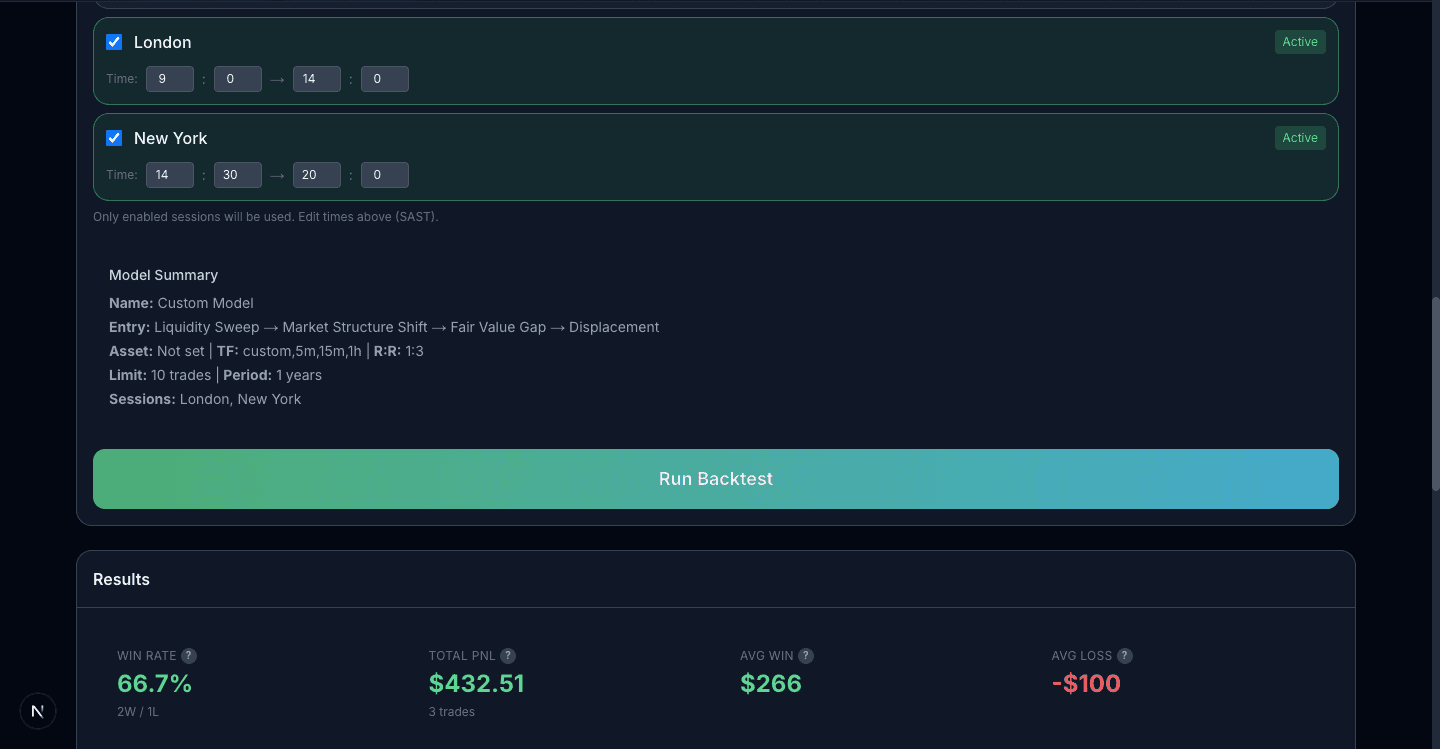

Set account size, risk per trade, slippage and commission, then gate entries by high-impact news, DXY alignment and session kill zones (London, New York, Asia — in SAST).

4

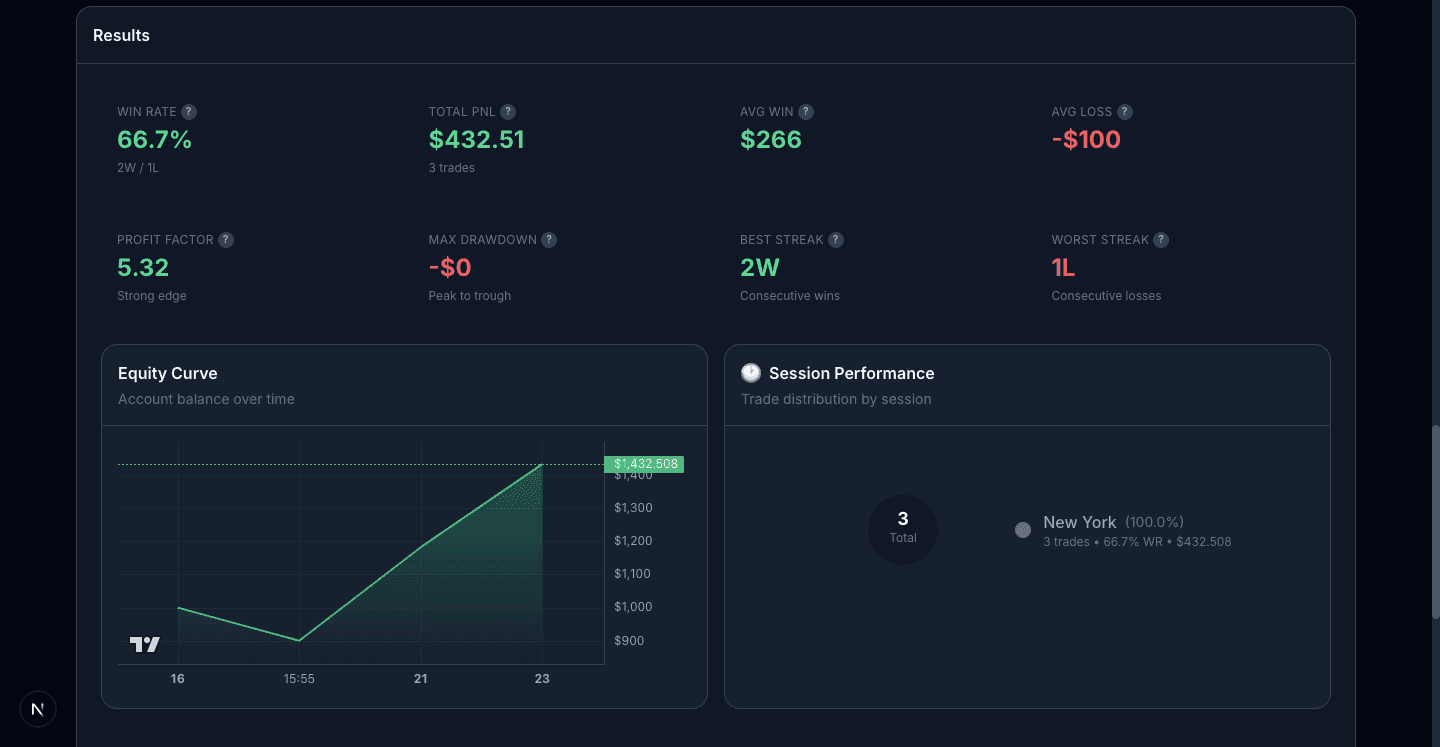

Results Dashboard

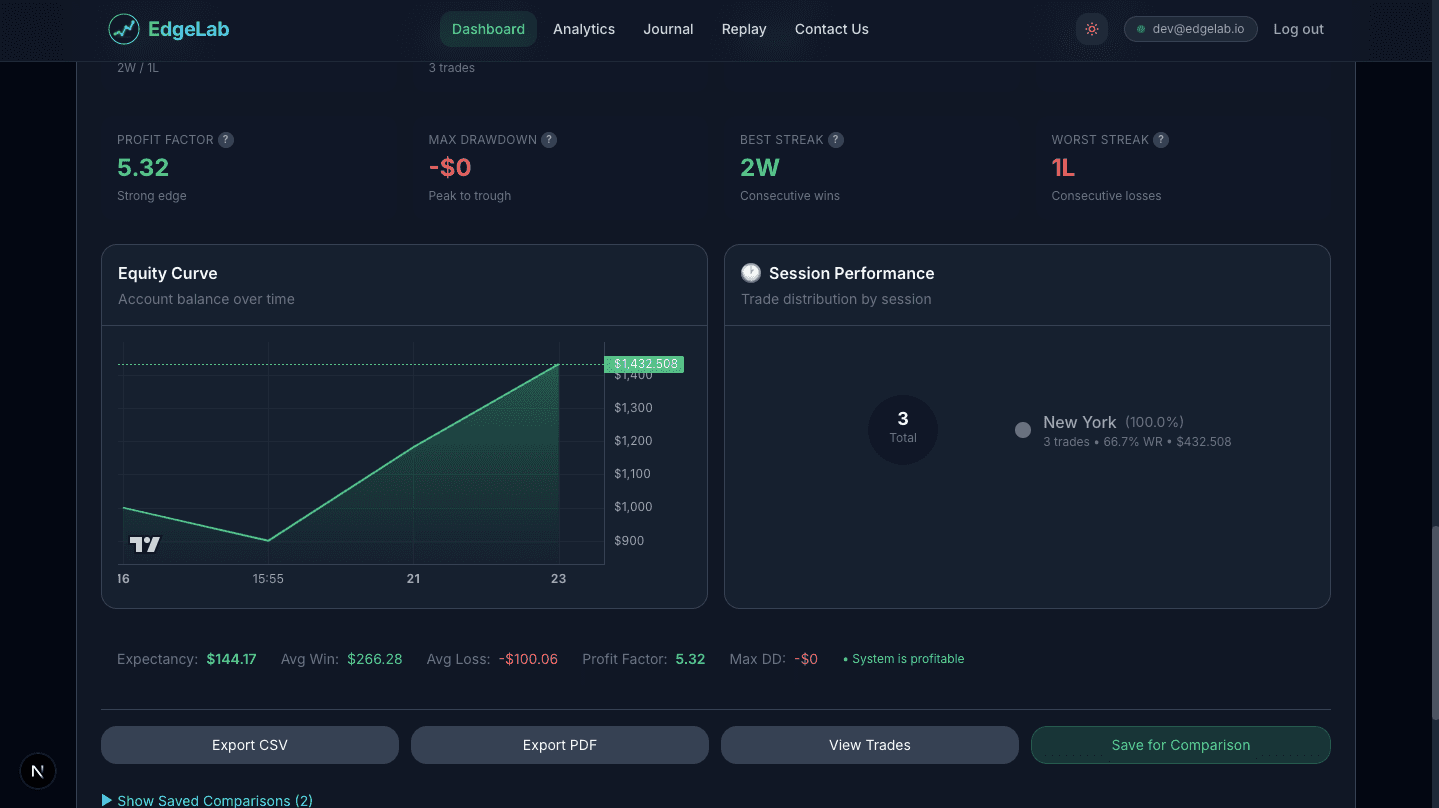

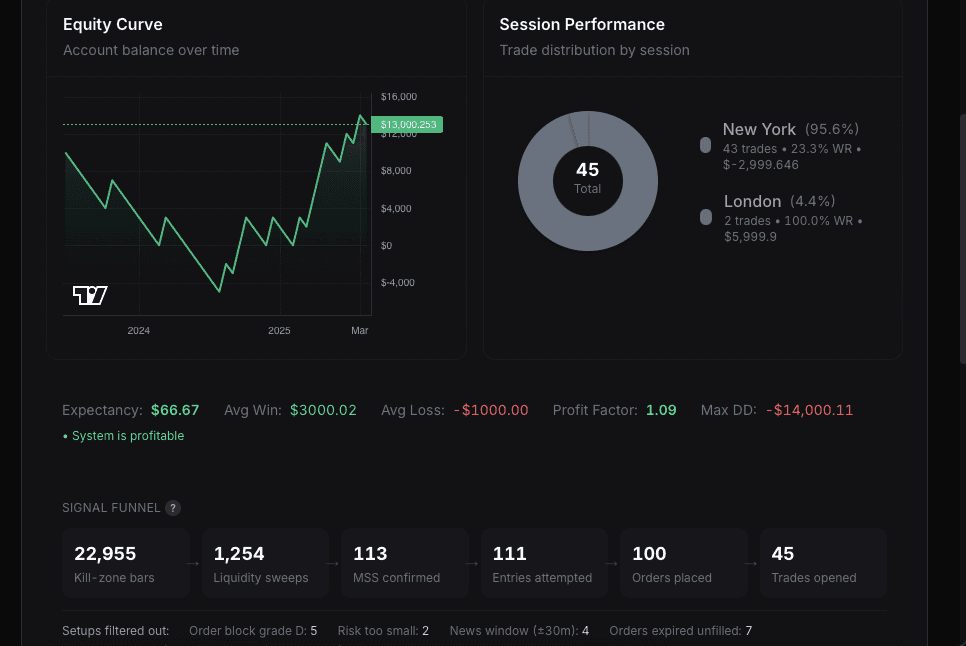

The honest verdict: 26.7% win rate (12W / 33L), +$3,000.25 net P&L and a 1.09 profit factor — profitable on a 1:3 R:R, not on hit-rate. Drawdown, streaks and session split are all on the table.

5

Equity Curve & Sessions

Account balance over time alongside a session breakdown — New York carried 43 of 45 trades, while the model's edge clustered in specific conditions rather than across the board.

6

Signal Funnel & Market Context

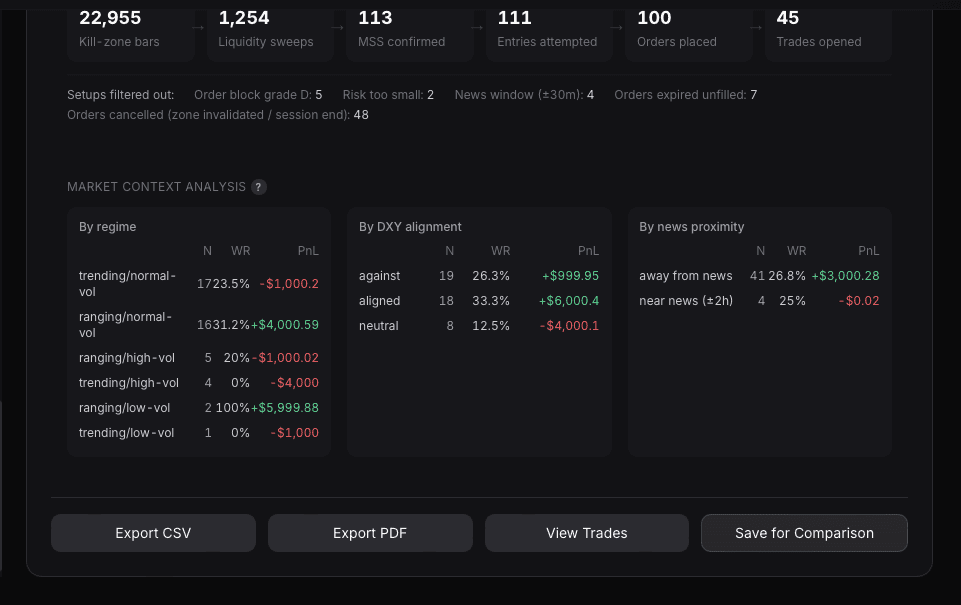

A 6-stage funnel — 22,955 kill-zone bars → 1,254 liquidity sweeps → 113 MSS → 111 entries → 100 orders → 45 trades — plus performance sliced by volatility regime, DXY alignment and news proximity.

The Challenge

Our client was manually backtesting Smart Money Concepts (SMC) strategies on TradingView. This process was slow, prone to human error, and impossible to scale. They needed a way to scientifically validate their edge across multiple currency pairs and timeframes without spending hundreds of hours on manual replay.

The Solution

We engineered a custom Python/FastAPI backtesting kernel wrapped in a Next.js dashboard. The engine walks the price series bar by bar, simulates realistic execution (slippage, commission, unfilled and expired orders), and resolves the full SMC chain — Liquidity Sweep, Market Structure Shift, Fair Value Gap, Order Block and Displacement — through a transparent 6-stage signal funnel.

Crucially, it doesn't just spit out a win rate. Every trade is tagged with its market context — volatility regime, DXY alignment and news proximity — so the trader can see where an edge actually lives. The frontend is an interactive command center: adjust any parameter and instantly re-read the equity curve, session split and full performance breakdown.

Built for Real Trading

- Realistic execution — slippage, commission, and orders that expire or go unfilled. No inflated backtests.

- Session-aware execution with configurable kill zones (London, New York, Asia)

- Multi-asset — XAUUSD, EURUSD, GBPUSD, USDJPY, BTCUSD and DXY

- Market-context tagging by volatility regime, DXY alignment and news proximity

- Export to JSON and Pine Script for live deployment

Key Technologies

Next.jsReactFastAPIPython / pandas / numpySupabaselightweight-chartsTailwind CSS

Project Outcomes

- Eliminated manual chart replay completely

- Any model validated across 70,000+ bars in seconds

- Surfaced the model's true edge — profitable at a 26.7% win rate on 1:3 R:R

- Pinpointed where the edge lives: by session, regime, DXY alignment and news

- Exportable to JSON and Pine Script for live deployment

"We went from spending weekends manually replaying charts to validating any strategy in seconds. This changed how we trade."

— Client, Private Trading Firm

Need a Custom Trading Tool Built?

We specialize in building high-performance fintech applications — backtesting engines, analytics dashboards, and automation tools for traders and funds.